The olive oil market is moving away from the most critical phase of the last two campaigns, yet the new scenario is not one of true normality. According to the market analysis presented by Annachiara Saguatti of Areté during PR Italia Edizioni’s Digital Round Table in Madrid, the sector is entering a more balanced phase, but one still shaped by structural volatility, weather risk and fragile inventories.

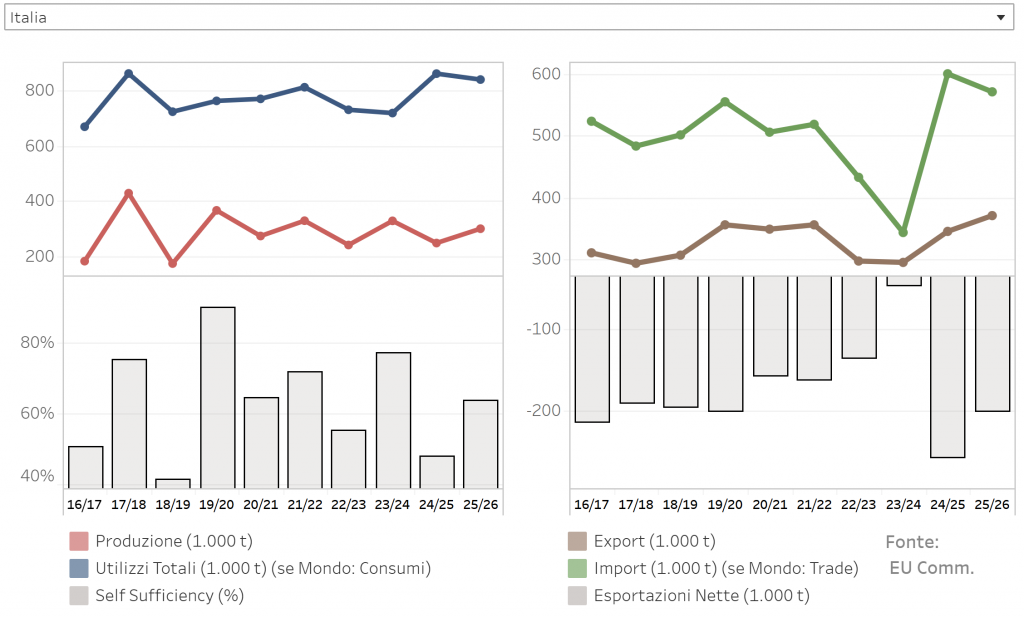

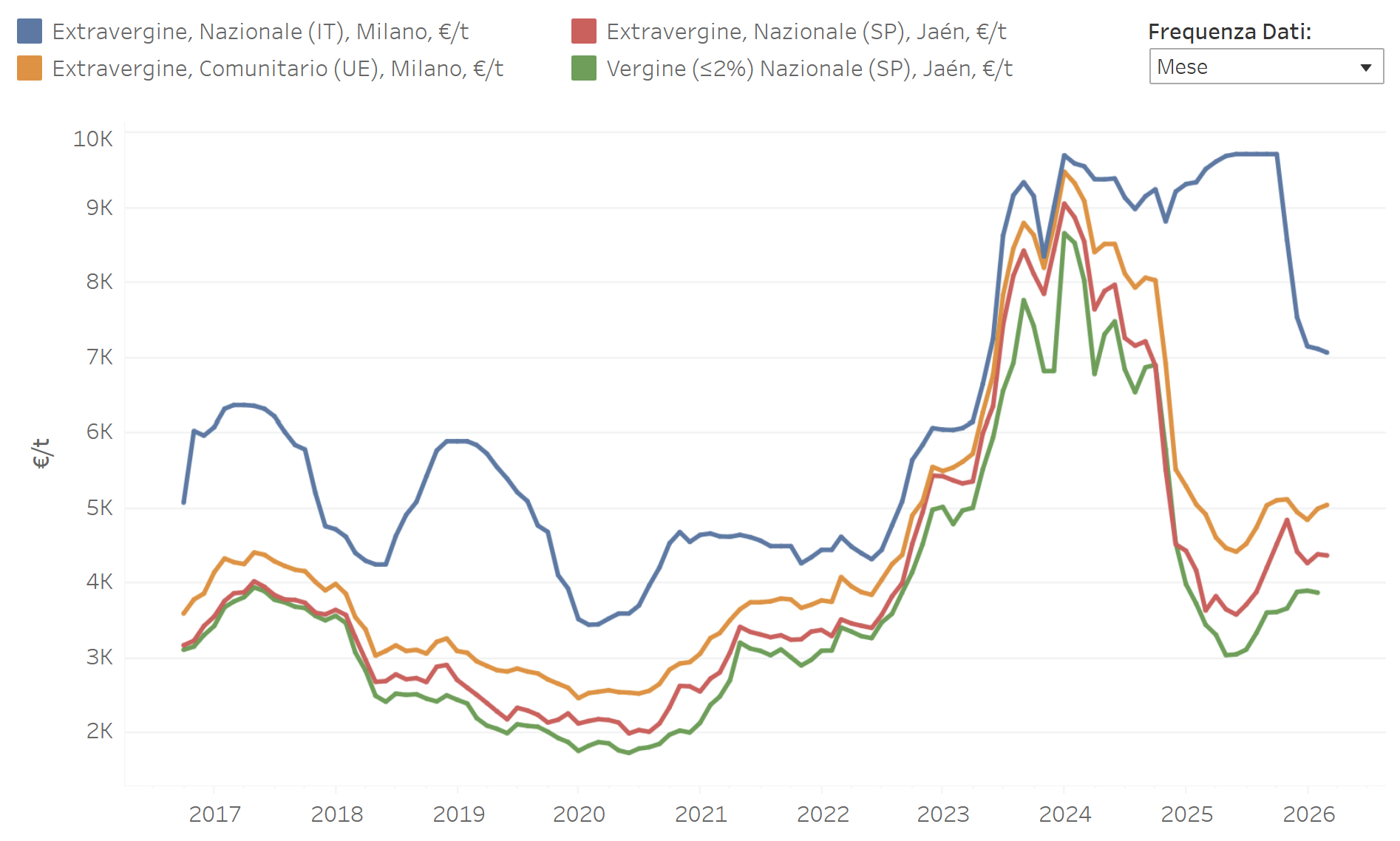

Italy is showing a meaningful production recovery in the current campaign, with output estimated at around 300,000 tonnes. This improvement has contributed to a significant correction in Italian extra virgin olive oil prices compared with the exceptional highs seen in recent months. However, this is not a return to low historical levels. Italian EVOO still trades above the peaks reached in previous low-supply campaigns, confirming that quality Italian oil continues to operate within a premium framework.

That point is particularly important for premium-oriented markets. Price normalization should not be mistaken for commoditization. What the market is witnessing is a partial easing of pressure, not a loss of value for Italian origin. In fact, the underlying fundamentals continue to support the strategic positioning of Italian extra virgin olive oil in the high-end segment: limited structural supply, strong origin recognition, and a global reputation built on traceability, sensory profile and food culture.

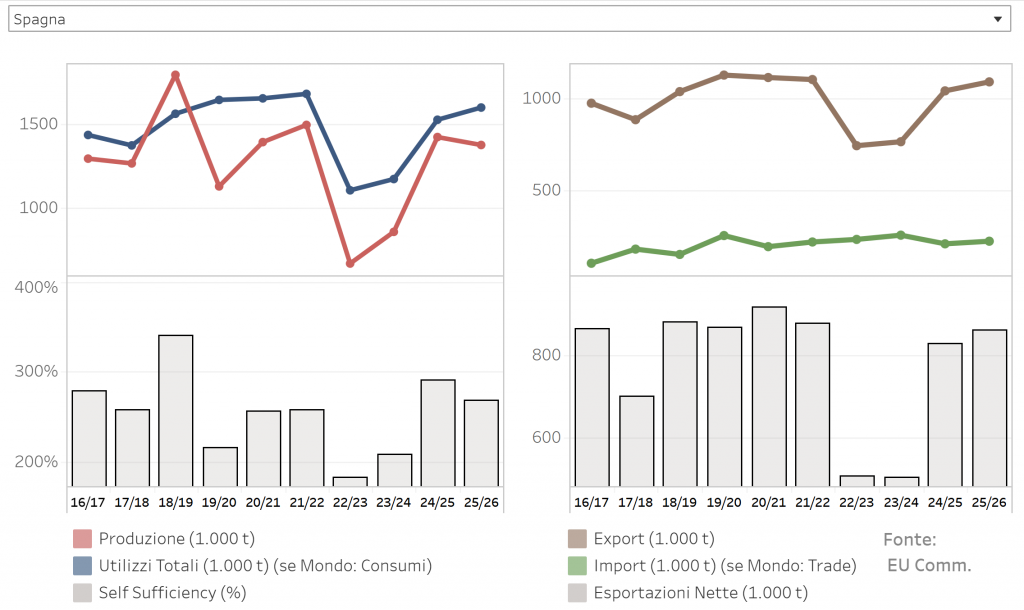

By contrast, the broader EU market remains highly dependent on Spain. Spanish production continues to be the main benchmark for Mediterranean and international pricing. Early expectations for the 2025/26 Spanish campaign were optimistic, supported by strong spring rainfall, but weather conditions later became more complex. Reduced precipitation, high temperatures and harvesting delays have all contributed to uncertainty. Areté suggests final Spanish production may end closer to 1.3 million tonnes rather than the higher official estimate, a reminder that even in a better year the market remains vulnerable to sudden revisions.

This matters because inventories across Europe are still not particularly comfortable. Italy may be recovering production, but stocks remain below historical averages, and Spain is rebuilding availability more slowly than expected. In other words, the market is less stressed than before, but far from oversupplied.

That is where Tunisia enters the picture. With production exceeding 400,000 tonnes, Tunisia is playing an increasingly relevant role as a supply buffer for the European market. Its strong export performance is helping contain upward pressure in the broader extra virgin segment. Yet this growing availability should be read carefully from a premium perspective: additional volume may stabilize the market, but it does not replace the positioning of Italian oil where origin, quality perception and culinary identity are key purchase drivers.

For importers, distributors and premium retailers around the world, the current phase presents a more nuanced opportunity. On one side, lower tension in the market may create better procurement conditions than during the previous crisis years. On the other, Italian extra virgin olive oil remains a category where value is not defined by volume alone. The premium is still justified by scarcity, by origin, and by the ability of Italian producers to deliver recognized quality in a market increasingly crowded with alternatives.

Looking ahead, the outlook remains mixed. Italy could return to a lower-output cycle next season, in line with its traditional alternation pattern, while Spain’s future trajectory is still too uncertain to define with confidence. This means that premium buyers should avoid reading the current market as a long-term reset. A temporary easing in prices does not eliminate the strategic importance of securing high-quality Italian supply.

For the global premium segment, the real takeaway is this: the olive oil market may be calmer, but Italian EVOO continues to stand apart. In a world where volatility is becoming structural, quality, traceability and origin are not optional attributes. They are the real drivers of long-term value.